The First Court Judgment in Mainland China on Transgender Insurance Rights: AIA’s Unlawful Termination of Contract

Cite this article 引用本文

@online{2025-08-en-2025-vs-aia,

author = {{Carolyn Sun}},

title = {The First Court Judgment in Mainland China on Transgender Insurance Rights: AIA’s Unlawful Termination of Contract},

year = {2025},

url = {https://carolyn.sh/blog/en/2025-vs-aia},

urldate = {__URLDATE__}

}Even if your processes and legal compliance are impeccable, AIA may still render an unjust decision regarding your policy. Should you prevail in court, insurance agents might disseminate misleading narratives on social media to tarnish your reputation. AIA has trampled upon its professed values and fundamental business ethics, exposing a veneer of hypocrisy and insincerity in matters of social responsibility.

Timeline

2023

In December, the insurance contract was duly executed, with the policyholder’s particulars designating a male identity, and I had already apprised the insurance agent of my gender identity, transgender status (male to female), and possible medical history and treatment.

2024

In January, I made the payment as agreed, and the insurance contract came into effect.

In July, I underwent gender affirmation surgery (SRS).

In November, I obtained my female ID card in accordance with the law and submitted the relevant documentation to AIA, requesting an update to my client information.

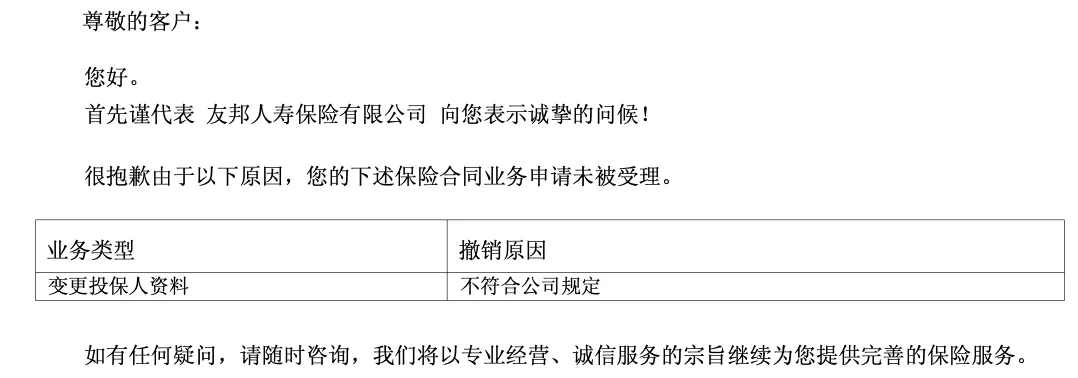

In December, AIA refused to update my client information, citing “non-compliance with company policy.” AIA then unilaterally terminated the insurance contract, claiming that “the insurance contract had not come into effect.” (Postscript: AIA’s company policies are quite powerful, seemingly superseding the law.)

2025

In February, after I filed a complaint with the Shanghai Branch of the National Financial Regulatory Administration (NFRA), AIA updated my client information but still refused to acknowledge the validity of the insurance contract, citing “policyholder’s concealing medication and medical history”.

In April, I filed a lawsuit seeking confirmation of the insurance contract’s validity and reimbursement for unpaid ordinary medical expenses.

In July, during the public trial, I (my lawyer) proved that all of AIA’s reasons for termination were untenable. The court ruled in my favor, confirming the continued validity of the insurance contract and ordering AIA to pay the unpaid ordinary medical expenses. AIA acknowledged the contract’s validity in court. AIA subsequently executed the judgment and did not appeal. Seven or eight AIA employees were present.

The court’s ruling was based on the spirit of contract law; if there were no grounds for termination, the contract would be upheld. “Gender affirmation” as a general practice does not need to be explicitly stated; emphasizing it could be seen as unfair. According to the law, insurers cannot unilaterally terminate contracts without cause, and all of AIA’s arguments were refuted by me (my lawyer) and dismissed by the court. The court conducted a lawful review and ruled in support of my claims.

After the trial, AIA requested that the court not make the judgment document public, but this request was denied.

In August, AIA met with me to explain the relevant matters. Several employees expressed verbal apologies, acknowledging improper conduct during the termination of the insurance contract and stating that they had improved the process for updating transgender identity information. AIA offered an ambiguous compensation of 200,000 (later increased to 300,000), hoping that I would waive my rights to disclose this matter to all institutions, media, and the public. According to Chinese law, such clauses are “invalid clauses”, so I rejected this proposal.

In September, I suffered from mental stress and contacted AIA, requesting that they restrain their employees from making distorted statements about this matter. However, AIA stated that this was a personal opinion of the employees and could not be restrained. Contradictorily, they also required me, as the party involved, to sign a statement waiving my rights to file complaints and reports. I knew that AIA could not deprive me of my legal rights to complain and report, so I refused this request. After careful consideration, I decided to make this matter public and submitted recordings of several meetings that restricted my civil rights to the relevant regulatory authorities.

In October, AIA informed me through its customer service that:

- The company has respected the court’s judgment and fully implemented the judgment content, as well as improved the relevant processes.

- The company has internally dealt with the relevant employees, who were responsible for the contract dispute.

- The company cannot make a formal apology and cannot restrain its employees’ statements about this matter.

Based on this statement, I have disclosed some recordings related to unfair treatment to several media outlets.

In the same month, some media reported on this matter and interviewed me and AIA. In the interview with journalists, AIA downplayed the issue, stating that it was a contract dispute case caused by my “failure to disclose honestly”. The company only wanted to reach a settlement through the judgment and did not mention the fact that it unilaterally terminated the contract. This statement deviated significantly from the facts recognized by the court’s judgment and misled the public’s understanding of the case. I made a solemn statement to AIA.

During this process, the journalists were also threatened by AIA’s public relations personnel.

Insurance Claims Record

I have strictly adhered to the terms of reimbursement in the insurance contract, and I have never applied for claims outside of the agreed terms, for pre-existing conditions, or for gender affirmation treatments. Below is my claims record for the entire year of 2024. It is evident that I am a very qualified and compliant insurance customer.

| 2024-mm-dd | Claim Amount (CNY) | Claim Reason | Claim Status |

|---|---|---|---|

| 3-23 | 2208.6 | Gastroenteritis consultation at luxury medical institution | Normal Claim |

| 6-15 | 1048.88 | Skin erythema consultation at luxury medical institution | Normal Claim |

| 9-22 | 999.2 | Ear canal inflammation consultation at luxury medical institution | Normal Claim |

| 10-18 | 640 | Dizziness and headache consultation at luxury medical institution | Normal Claim |

| 10-28 | 2205.6 | Dizziness and headache consultation at luxury medical institution | Claim obtained through litigation |

| 11-10 | 1260.82 | Dizziness and headache consultation at luxury medical institution | Claim obtained through litigation |

| 11-14 | 960 | Dizziness and headache consultation at luxury medical institution | Claim obtained through litigation |

| Amount Claimed Normally (CNY) | Claim Amount (CNY) | Policy Price (CNY) |

|---|---|---|

| 4896.68 | 4426.42 | 20746(23 years old - including outpatient and inpatient - global except the US - 0 deductible) |

Legal Details

It is important to emphasize that when purchasing the insurance policy, I fully disclosed my gender identity, transgender status, medications, and medical history to the insurance agent. During the contract period, I never filed any claims related to transgender-related medical treatments. The judge conveyed the view during the trial that gender reassignment surgery is a “normal” and “routine” medical procedure, and overemphasizing it is another form of discrimination. Therefore, I personally believe that the court’s focus is on the validity of the insurance contract as a contractual relationship.

Below are the questions I faced when discussing this case.

SRS surgery does not constitute grounds for contract termination

Prior to apprising AIA personnel of the company’s professed support for the transgender community as articulated in its ESG reports, the primary justification advanced by AIA for contract termination centered on the alleged profound ramifications of SRS surgery upon the insured’s health profile, thereby precipitating the contract’s dissolution.

The insurance contract does not stipulate a prohibition on SRS surgery. Therefore, SRS surgery itself does not constitute grounds for contract termination. Even if there were relevant provisions in the contract, AIA could not prove that SRS surgery had a substantial impact on the insured health status. In fact, SRS surgery is a common medical procedure that has been widely recognized and accepted in modern medicine. The National Health Commission (NHC) of China has also issued relevant technical specifications and guidelines. AIA expectedly failed to provide any evidence that the surgery would increase insurance risks or make contract performance difficult. Therefore, AIA’s termination of the contract on the grounds of SRS surgery lacks legal basis.

AIA failed to prove non-disclosure of mental disorders

AIA claimed in court that I had mental disorders such as depression before purchasing the insurance, constituting non-disclosure, and used this as a reason to terminate the contract.

I provided judicial appraisal and documents from a top-tier hospital’s psychiatry department before purchasing the insurance, proving that I had no mental disorders. AIA failed to provide any contrary evidence. Therefore, AIA did not receive the court’s support.

I did not conceal my past medication and medical history

AIA claimed in court that I had not disclosed my medication and medical history in advance, which constituted another form of non-disclosure.

I provided evidence that I had fully disclosed my gender identity and transgender status to AIA in advance, along with relevant medical information when purchasing the insurance. Therefore, AIA’s termination of the contract on the grounds of my failure to disclose this information in advance also lacks legal basis. Consequently, the court did not support AIA’s argument.

The contracting party has not changed

This argument is actually quite baffling. After the case became public, I received similar questions from other AIA agents who appeared to have little familiarity with basic contract law.

The contracting party has not changed. The change of gender information is similar to the change of name information, and the public security police will issue corresponding certification documents to prove the legality and validity of the change. Insurance companies should respect and recognize the identity information that the insured has legally changed, and should not terminate the contract on this basis.

According to Chinese law, if the subject of a party changes, the contract should naturally become invalid without the need for termination.

Updating personal identity information is a right granted to citizens by law and has legal effect within the Chinese legal system; the subject of personal identity has not changed as a result. AIA’s refusal to recognize the legally changed gender identity completely ignores the existing legal effect, and this practice not only violates the principle of equal treatment but also constitutes an infringement on personal dignity.

ESG Reports

It is worth mentioning that AIA has frequently mentioned its support for the transgender community in its ESG reports. Frankly speaking, it was this trust that led me to choose AIA’s insurance products. AIA even offers medical insurance products for transgender individuals in India. From my subjective experience, AIA lacks basic business ethics, and its actions are completely different from the values it claims to uphold. I did nothing wrong, did not conceal the truth, did not seek benefits beyond the contract, and even my annual reimbursement amount is less than half of the insurance premium. I feel very disappointed to suffer such unfair treatment.

2024

Within the Health and Wellness subsection of AIA Group’s 2024 ESG Report, AIA highlights its support for the transgender community and artistic initiatives in New Zealand, thereby exemplifying a profound respect and inclusivity toward multicultural diversity.

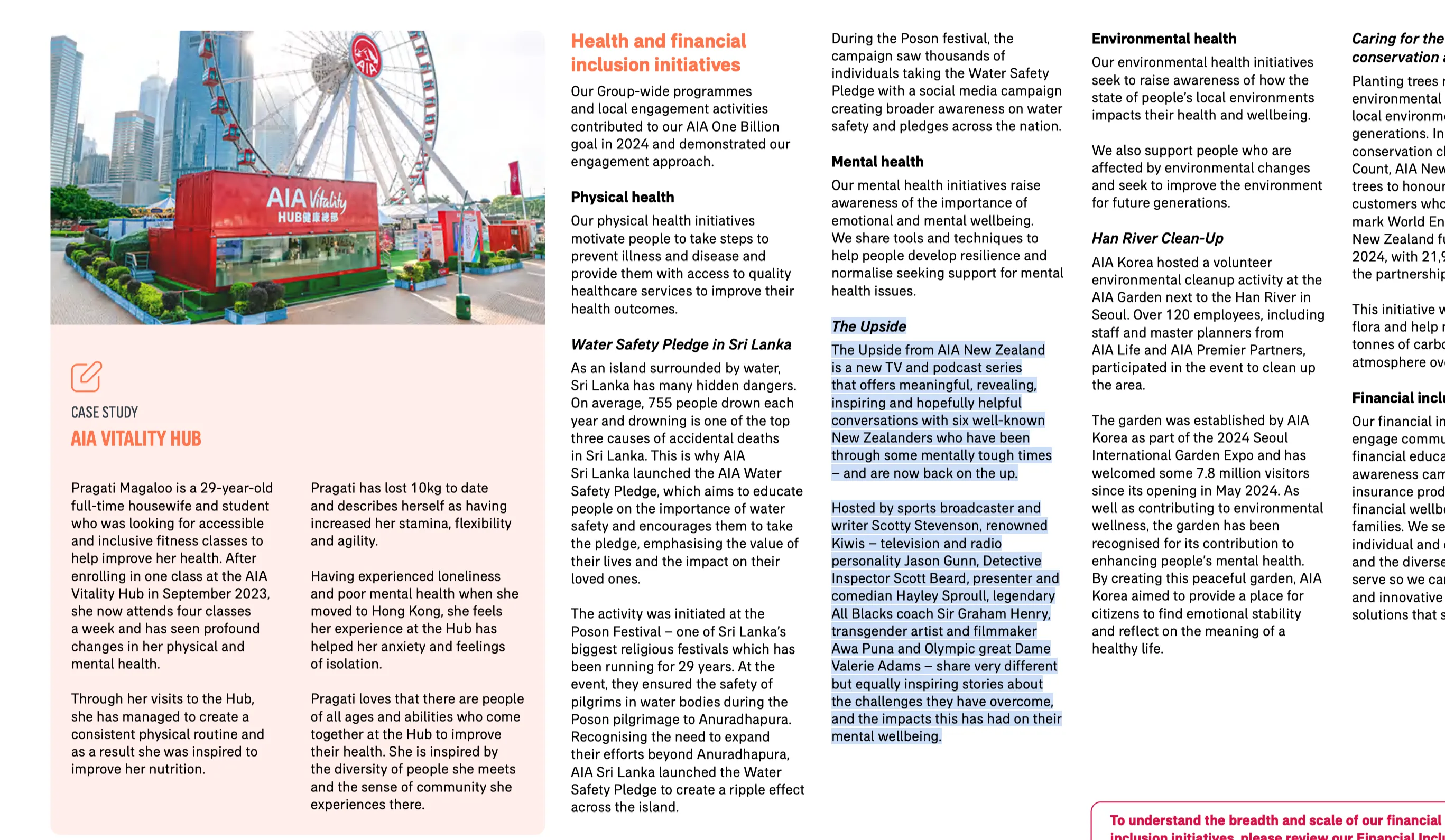

The Upside from AIA New Zealand is a new TV and podcast series that offers meaningful, revealing, inspiring and hopefully helpful conversations with six well-known New Zealanders who have been through some mentally tough times – and are now back on the up. Hosted by sports broadcaster and writer Scotty Stevenson, renowned Kiwis – television and radio personality Jason Gunn, Detective Inspector Scott Beard, presenter and comedian Hayley Sproull, legendary All Blacks coach Sir Graham Henry, transgender artist and filmmaker Awa Puna and Olympic great Dame Valerie Adams – share very different but equally inspiring stories about the challenges they have overcome, and the impacts this has had on their mental wellbeing.

2023

Within the Health and Wellness subsection of AIA Group’s 2023 ESG Report, AIA highlights its provision of medical insurance for transgender individuals in India and commits to continuing to offer medical insurance coverage for transgender individuals in the future.

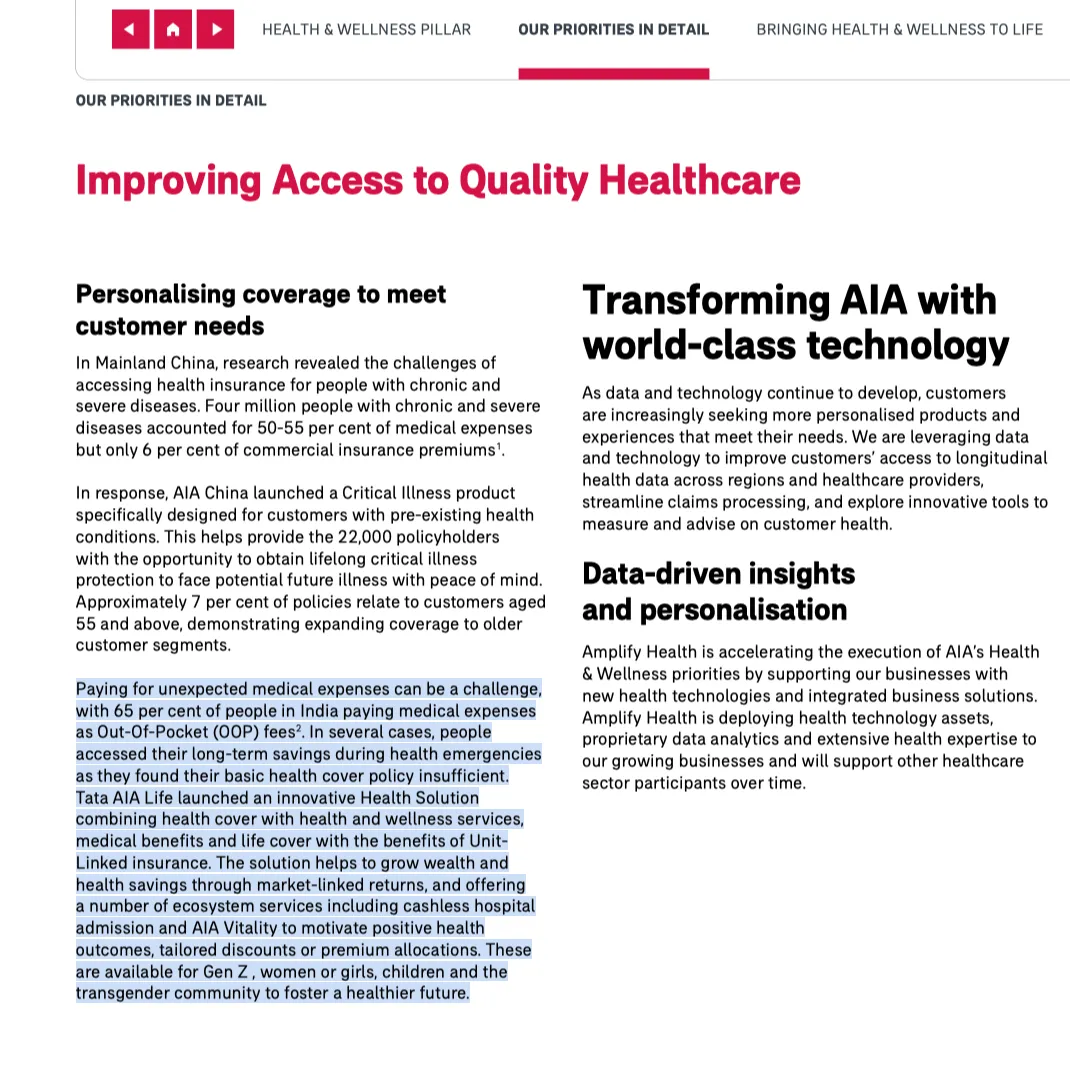

Paying for unexpected medical expenses can be a challenge, with 65 per cent of people in India paying medical expenses as Out-Of-Pocket (OOP) fees2 . In several cases, people accessed their long-term savings during health emergencies as they found their basic health cover policy insufficient. Tata AIA Life launched an innovative Health Solution combining health cover with health and wellness services, medical benefits and life cover with the benefits of Unit-Linked insurance. The solution helps to grow wealth and health savings through market-linked returns, and offering a number of ecosystem services including cashless hospital admission and AIA Vitality to motivate positive health outcomes, tailored discounts or premium allocations. These are available for Gen Z , women or girls, children and the transgender community to foster a healthier future.

Reflections

- In commercial insurance disputes, most consumers give up on litigation because it takes time and money. Cases that actually go to trial are rare, and publicly disclosed cases involving sexual minority plaintiffs are rarer still. I chose to see this through court not only to protect my own rights, but in the hope that it might help others facing similar situations.

- AIA’s unjustified termination of my policy was not only a violation of my rights as a policyholder, but a blow to public confidence in Shanghai’s financial sector. For most consumers, the cost and complexity of litigation make it easy to walk away from claims they have every right to pursue.

- Throughout this process, AIA treated my transgender status as grounds for termination while refusing to recognise the legal validity of my updated identity documents. This went beyond a contract dispute. The refusal to acknowledge my gender identity, the denial of routine claims without explanation, and the absence of any genuine remedial intent caused real and sustained psychological harm, in direct conflict with the protections of personal dignity enshrined in the Civil Code.

- Even if your processes and legal compliance are impeccable, AIA may still render an unjust decision regarding your policy. Should you prevail in court, insurance agents might disseminate misleading narratives on social media to tarnish your reputation. AIA has trampled upon its professed values and fundamental business ethics, exposing a veneer of hypocrisy and insincerity in matters of social responsibility.

Judgment Document and Media Reports

Judgment Document

Media Reports

[HK01] 01獨家-上海跨性別者狀告友邦保險無故解約-內地首宗判決出爐

[信网] 投保人性别重置后保险被退医疗费拒赔 法院判友邦人寿全额赔付

[信网] 信号山:别让「躺平式拒赔」成了「友邦保险们」的逐利哲学

EOF